It was not just Bond Market Vigilantes at work sending messages on tariffs. Investors had placed faith in the “Trump Put,” or the idea that a falling stock market would keep guardrails on economic policy. During the first Trump administration, when stock market performance was frequently cited as a barometer of policy success, the S&P 500 declined 18% in Q4’18 amidst escalating China tariff headlines, including a 19% peak to trough drop (2924 to 2351). The rhetoric subsequently receded. This time? The S&P 500 reached 6145 back on Feb. 19, and closed Tuesday April 8 at a low of 4982: down 19%! The following day, the index was 10% higher as tariffs were paused 90 days. While the bond market was cited, stocks also sent a message on policy that seems, for now, to have been received.

How did the sudden market moves shift the market’s risk compensation and, more importantly, what can it say about its status going forward? Just as with bonds in the prior outlook article, we can use our tools.

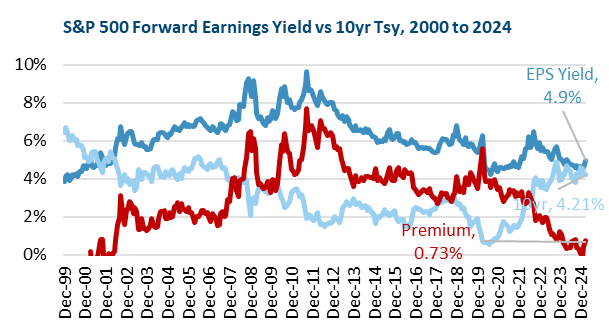

Chart 1

Chart 1 shows the earnings yield on the S&P 500, the yield on the 10yr Treasury, and the difference between the two, known as the Equity Premium. A higher Equity Premium means stock investors are getting more compensation relative to bonds. From 2002 to 2007, prior to the Fed’s QE interventions, a 1-3% Equity Premium was common.

On March 31, when Q1 ended, the Earnings Premium was 0.73%: better than 0% at the start of the year, but below the 2003-2007 range of 1.50%-2.50%. By April 4, with 10yr yield 30 bps lower, at 3.90%, and the earnings yield 10% higher at 5.5% (because the S&P is 10% lower), you get an earnings yield of 1.60%, more than double the end of the quarter just two days prior, and into the 2003-2007 range. In the subsequent week, bonds lost about 2%, while the S&P 500 gained 6%. As of April 11, the Earnings Yield is back to 5.1%, while the 10yr is at 4.47%. The Earnings Yield is back to 0.7%, the same level as the start of the quarter. But the key insight here is that, of the 90 bps decline, the majority was from the 10yr rising nearly 60 bps, and just 30 bps from the S&P 500 increase.

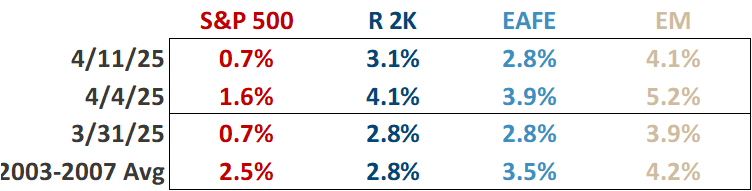

The same analysis can be performed on the other major indices. Earnings yields on all markets improved from March 31 to April 4, but have since reversed. While the S&P 500 and EAFE have fully recovered, the Russell 2000 and MSCI EM are still above their March 31 levels. More importantly, the Russell 2000 values are above their 2003-2007 averages, while EAFE and EM are in line (see Chart 2). This is a reminder that these other parts of the equity markets have valuation appeal.

Chart 2

It is important to remember that the tariff risk is a reversible, not irreversible, problem. The Russell 2000 would be the biggest potential beneficiary of tariff headlines fading and focus returning to the prospect of a growing U.S. economy. The MSCI EM would also benefit from clarity on what the actual expectations for countries in the global supply chain are. The S&P 500 and MSCI EAFE represent larger companies with greater resources to manage a period of trade uncertainty. Still, the MSCI EAFE could benefit as the home of greater perceived policy stability, while the S&P 500, the home of many extremely successful businesses built on the foundation of global trade, would benefit as well. Yet, the S&P 500’s higher valuation and businesses reliant on global supply chains makes it vulnerable to a more drawn-out process.

What Do Stocks Discount? If we get a stagflation scenario of upward pressure on interest rates AND uncertainty or pressure on profits, that would be a headwind for both stocks and bonds, and thus diversified investor portfolios. On the other hand, if the uncertainty that currently is surrounding the tariff fight continues to abate, confidence in stock profits (and growth), plus a downtick in yields, would support both pillars of client portfolios. After a quarter (plus a week) driven by tariff headlines, it appears that the remainder of Q2, at least, will be driven by this. Ideally, tariffs will serve their desired purpose: Create negotiating leverage with other countries to level the playing field for trade and, somewhat ironically, spur more widespread free trade. The risk is trade deficits themselves are viewed as the problem, and the combination of lower growth and higher inflation that a protracted trade war would bring creates pressure for both the equity and fixed income portions of client portfolios.

Most importantly, it is a reminder for investors to have portfolios constructed to manage unexpected events which, by their very name, cannot be anticipated. It is also important to remember that many traders in volatile markets operate under shorter-term motivations than the long-term time horizons of the average investor, and that can exacerbate price moves.

The first step is having adequate portfolio liquidity for either income distributions or planned expenses, so that liquidity needs do not force poorly timed portfolio moves. The second is having a diversified portfolio with a variety of investments and strategies that will move differently in response to an unexpected shift in the macro backdrop. In other words, the somewhat boring advice of having a properly diversified portfolio with adequate liquidity for short term needs remains the best plan. And if an investor has such a portfolio, then the day-to-day noise, no matter how loud it may grow, does not require any sudden changes.

See Also:

- 3/31/25 Outlook Theme #1: Stop and Go Tariffs

- 3/31/25 Outlook Theme #2: Bond Market Vigilantes Send a Message

- Keep a Long-Term Perspective During Dark Days

Important Disclosures:

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Grimes & Company, LLC [“Grimes]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from Grimes. No amount of prior experience or success should not be construed that a certain level of results or satisfaction if Grimes is engaged, or continues to be engaged, to provide investment advisory services. Grimes is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the Grimes’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.grimesco.com. Please Remember: If you are a Grimes client, please contact Grimes, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian. Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Grimes account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Grimes accounts; and, (3) a description of each comparative benchmark/index is available upon request.

The information contained herein is based upon sources believed to be true and accurate. Sources include: Factset Research Systems Inc., Bureau of Economic Analysis, Bureau of Labor Statistics, Congressional Budget Office, Board of Governors of Federal Reserve System, Fred: Federal Reserve Bank of St. Louis Economic Research, U.S. Department of the Treasury

-The Standard & Poor’s 500 is a market capitalization weighted index of 500 widely held domestic stocks often used as a proxy for the U.S. stock market. The Standard & Poor’s 400 is a market capitalization weighted index of 400 mid cap domestic stocks. The Standard & Poor’s 600 is a market capitalization weighted index of 600 small cap domestic stocks.

-The NASDAQ Composite Index measures the performance of all issues listed in the NASDAQ stock market, except for rights, warrants, units, and convertible debentures.

-The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of 21 emerging markets. The MSCI All Country World Index is a free float adjusted market capitalization index designed to measure the performance of large and mid and cap stocks in 23 developed markets and 24 emerging markets. With over 2,800 constituents it represents over 85% of the global equity market.

-The Barlcays Aggregate Index represents the total return performance (price change and income) of the US bond market, including Government, Agency, Mortgage and Corporate debt.

-The BofA Merrill Lynch Investment Grade and High Yield Indices are compiled by Bank of America / Merrill Lynch from the TRACE bond pricing service and intended to represent the total return performance (price change and income) of investment grade and high yield bonds.

-The S&P/LSTA U.S. Leveraged Loan 100 is designed to reflect the largest facilities in the leveraged loan market. It mirrors the market-weighted performance of the largest institutional leveraged loans based upon market weightings, spreads and interest payments.

-The S&P Municipal Bond Index is a broad, comprehensive, market value-weighted index. The S&P Municipal Bond Index constituents undergo a monthly review and rebalancing, in order to ensure that the Index remains current, while avoiding excessive turnover. The Index is rules based, although the Index Committee reserves the right to exercise discretion, when necessary.

-The BofA Merrill Lynch US Emerging Markets External Sovereign Index tracks the performance of US dollar emerging markets sovereign debt publicly issued in the US and eurobond markets.

-The HFRI Fund of Funds index is compiled by the Hedge Funds Research Institute and is intended to represent the total return performance of the entire hedge fund universe.